Lobbyist Wars and the Development of BIM. Part 5: ⚈BlackRock — the Master of All Technologies. How Corporations Control Open Source.

Tech giants use investment fund money to control an increasing proportion of new developers and products, thus blocking the path for new programs and new technologies in the construction industry.

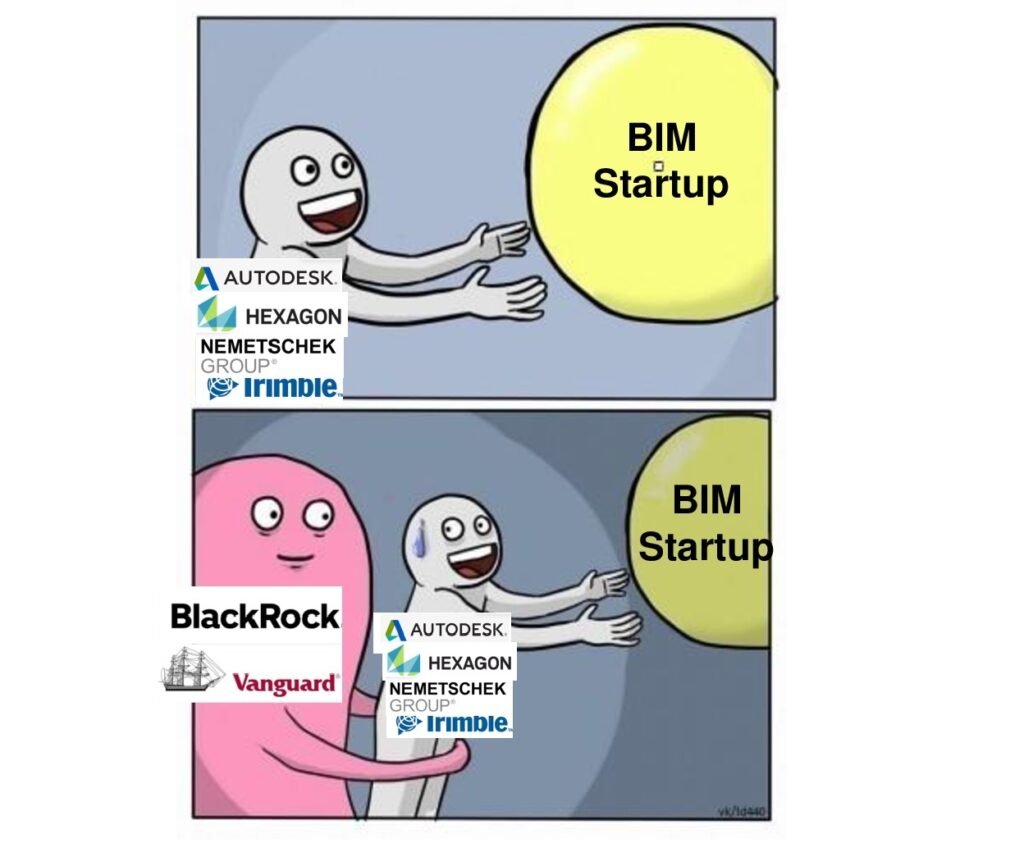

Today’s leaders in the CAD industry — Autodesk, Hexagon, Nemetschek, Bentley, Trimble — are well prepared for future threats: the standard tactic of large corporations has become aggressively capturing new markets and absorbing potential competitors in the early stages of development.

As a result, the entire CAD industry has become an oligopoly dominated by a group of several companies. And their position at the top is becoming more and more unshakable.

Content:

⚈ BlackRock — the master of all technologies

⚈ Oligopoly in the CAD market

⚈ Autodesk is following in Oracle’s footsteps

⚈ Why programs don’t develop

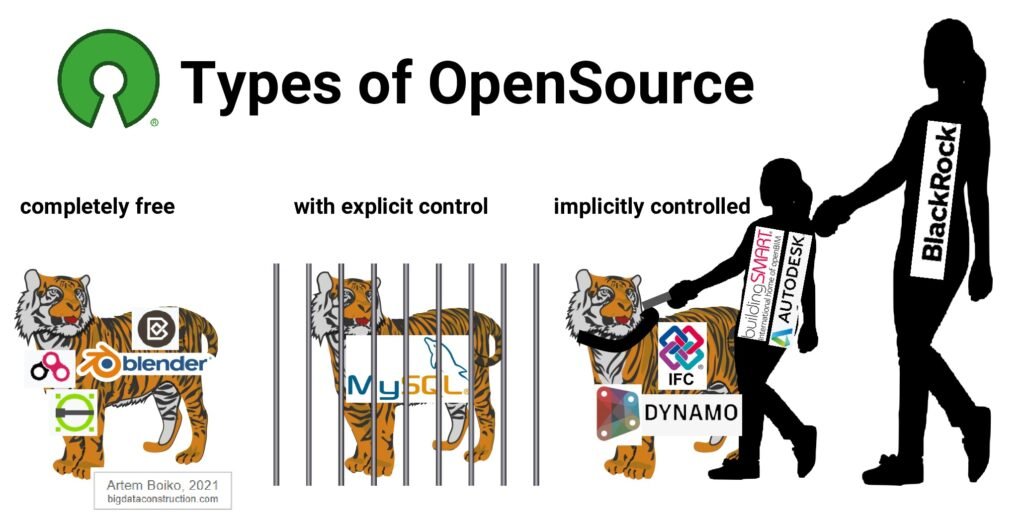

⚈ The corporation’s fight against open source

⚈ Autodesk and IFC data format

⚈ Autodesk Challenge — Open Standards Organization — ODA

⚈ In conclusion

BlackRock — the master of all technologies

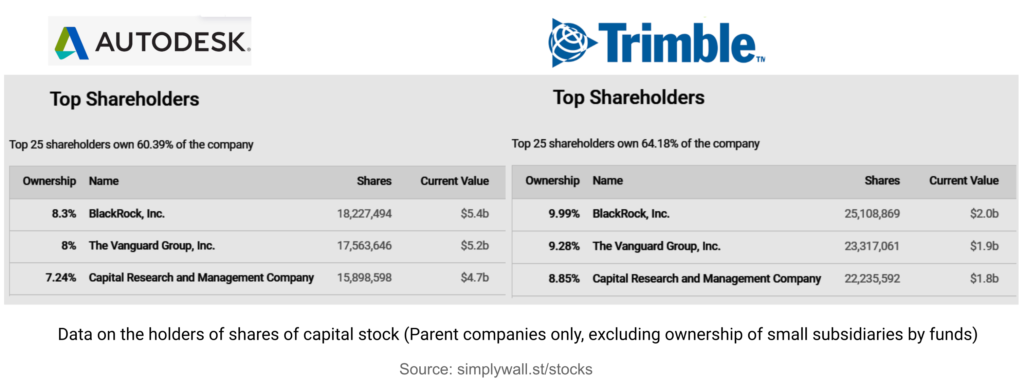

The basis of the oligopolistic structure in construction design is the big five CAD vendors: Autodesk, Hexagon, Trimble, Bentley, Nemetschek.

These companies went out from the mid-90s to an IPO (initial public offering), selling most of their shares among the largest investment funds in the United States and thereby distributing responsibility for the future of the companies among the shareholders.

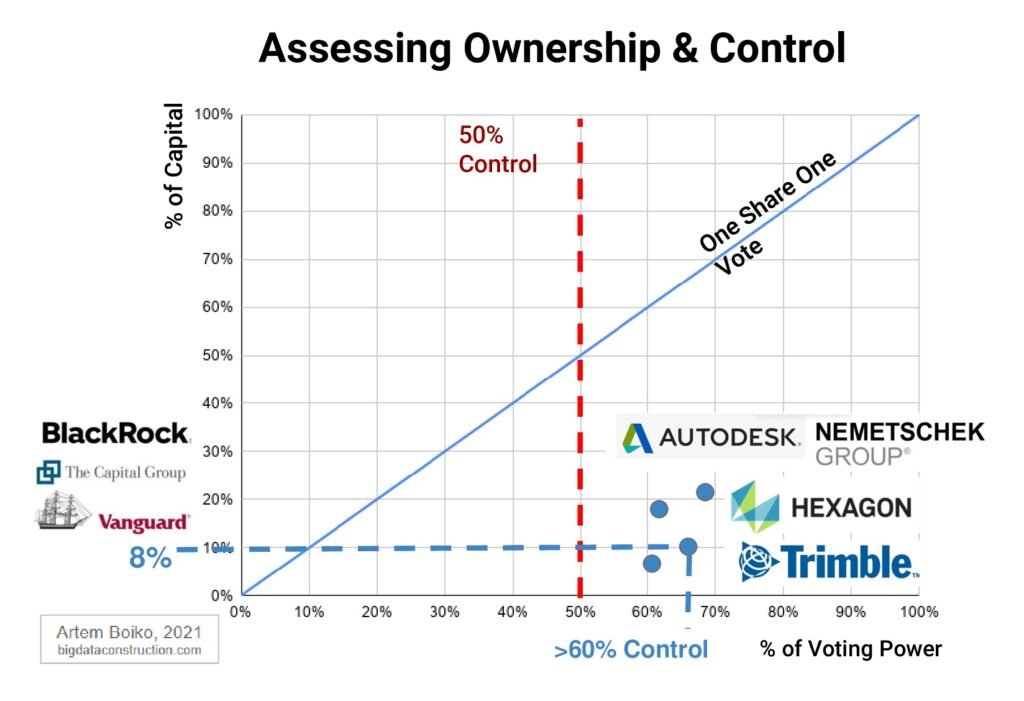

Data on the holders of shares in the authorized capital (only parent companies, excluding the holding of funds of small subsidiaries)

Three American investment funds, The Capital Group, Vanguard, and BlackRock, have been the main beneficiaries (and shareholders) of CAD companies going public, and over the past 30 years have bought technology stocks directly or through their bank branches.

Few have heard of BlackRock, but the firm is the largest investment firm, with $ 8.7 trillion in assets under management in 2021 (up from $ 4.6 trillion in 2015). For 2021, BlackRock, headquartered in Manhattan, has offices in 100 countries and is closely associated with major financial regulators such as the US Treasury, the US Federal Reserve System (FRS) and the European Central Bank (ECB).

As soon as a major economic entity comes to the attention of funds like Vanguard and BlackRock, they offer it profitable investment opportunities. Using their solid reputation, connections and huge funds, Vanguard and BlackRock buy up the assets of the subject and begin to manage it.

For example, in Germany alone in 2014, BlackRock owned 4% of BMW, 5.2% of Adidas, 7% of Siemens, 6% of Daimler. In general, BlackRock is a shareholder (almost always the largest) of all companies included in the DAX index (Germany’s most important stock index). BlackRock’s gigantic asset management platform Aladdin monitors the value of stocks, bonds and other assets under the company’s management every second, as well as calculates how various events, such as the rise in oil or aluminum prices, affect their prices.

BlackRock is the majority shareholder in nearly every technology company in the world. How are BlackRock and Vanguard (Vanguard / Windsor) investment corporations related to construction and engineering?

BlackRock and Vanguard own nearly every CAD and technology company in the world of civil engineering and BIM solutions.

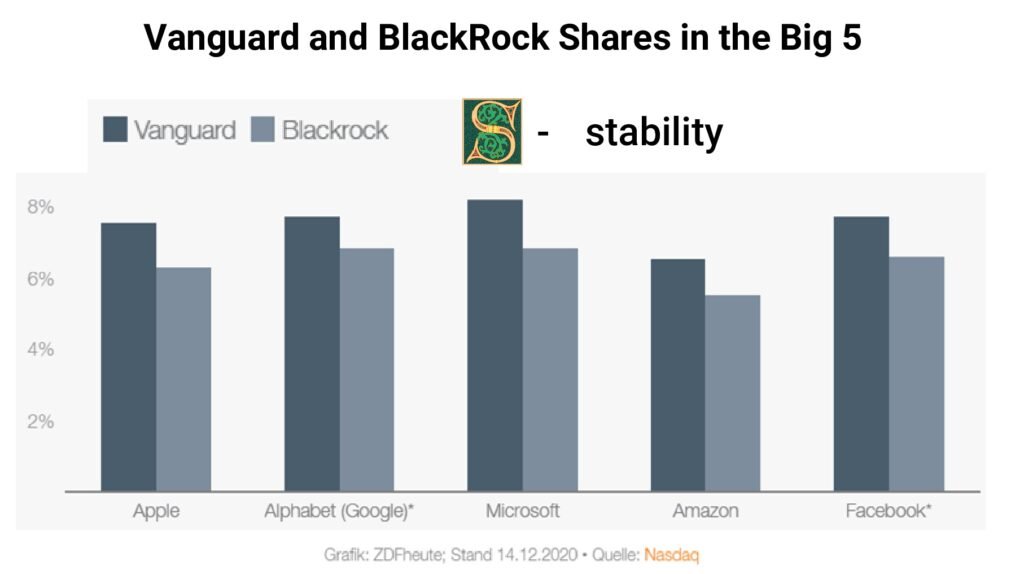

On the shareholding chart, it is noticeable that the numbers — 7–10% — have a special meaning here. Investment funds bring the share of ownership of any company to such numbers, which is enough to fully control entire corporations.

The following chart shows a similar distribution of shareholdings in the largest companies in the world — Big 5.

Due to the fact that 70% of the company’s shares after entering the stock exchange are distributed among thousands of investors, the controlling stake is only 7–20% of the shares, which gives the holder of the “small package” the authority to make all decisions in the company.

Thus, if you own 7–20% of the shares of several major monopoly companies, then you almost completely influence the development of the entire industry.

With such multiple cross-ownership and the presence of stakes in almost all large corporations — how do these investment funds manage to follow the BIM topic or, for example, the development of AR in construction, and indeed all the world’s technologies at the same time?

Oligopoly in the CAD market

Oligopoly primarily means coordination and interconnection in the activities of the market, which is carried out by Vanguard and BlackRock through the heads of the companies approved at the shareholders’ meeting.

Since entering the stock exchange, large CAD companies have actually killed the competition in the CAD market by the fact that the main strategic decisions are now made not by aggressive company leaders who are fighting for survival and a place in the market, but by a lobbied board of directors, which is controlled from the outside by financial specialists interested in the construction industry only as a figure in the Annual Revenue.

Political scientist Jan Fichtner of the University of Amsterdam, examining these major financial players, argues: “Influence is mainly carried out through background discussions. You are being led by BlackRock and Vanguard because you know that one day you may need their favor. It is rational for the management of companies and corporations to act in the interests of the main shareholders. “

“Where there is a treaty, there is a penknife.”

Charles-Maurice de Talleyrand-Perigord

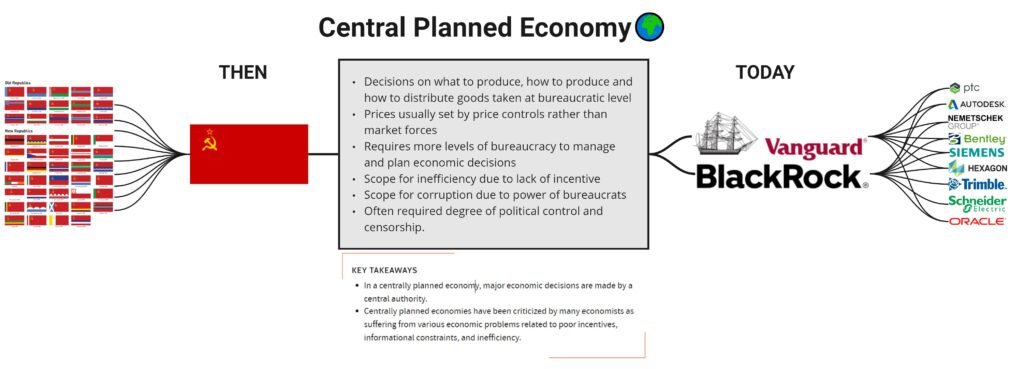

Everyone who works in the development of technology in the construction industry is gradually falling into the millstones of this planned economy, created by the sharks of capitalism with the support of wealthy dynasties of the West, pension funds and the Fed printing press.

BlackRock manages assets centrally and strictly enforces all formal regulations. But beyond that, BlackRock and Vanguard do almost nothing. Meanwhile, for the functioning of a market economy, it is extremely important that shareholders constantly keep their finger on the pulse of events in their enterprises and critically assess management policies.

As a result, today all the world’s CAD (and in general all technology) companies belong to investment funds, which on paper manage the company’s strategy, and de facto only comply with the formal requirements for reports, which later fall into a beautiful PDF document for the annual meeting of the board of directors.

“A planned economy on the scale of any large industrial system requires significant centralization and, consequently, a bureaucratic apparatus capable of managing this centralized machine. If planning from the top is not combined with active participation from below, if the flow of social life does not constantly ascend from the bottom up, the planned economy will lead to a new form of manipulation of the people.”

“Escape from Freedom” by Erich Fromm

How will Trimble compete with Autodesk or Hexagon in the same market today if the CEOs of these companies report quarterly to the same investment funds from WallStreet, which, in turn, are not interested in drastic changes in the markets on which their annual reports depend and, as a result, their personal bonuses.

Thus, fund managers have no financial incentive to compete fiercely with companies in their portfolios. If, for example, an active investor who owns, say, shares in Coca-Cola Co., but not PepsiCo Inc. may want Coca-Cola to take a big risk to crush Pepsi by investing in new products and markets, then on the other hand, an investor with both would prefer Coke and Pepsi to avoid price wars.

This relationship may not always be kind. A 2018 study found that when the same institutional investors are the largest shareholders of branded and generic drug companies, generic companies are less likely to offer cheaper versions of branded drugs. As a result, consumers can pay higher prices for medicines.

If there is no healthy competition, there will be no new technologies either. This is partly why all the big corporations in the construction design world have had virtually no involvement with new product development in the past 20 years.

If ten years ago such large companies as Autodesk, Nemetschek, Trimble had a reputation not as innovators, but rather as imitators, when it was enough just to copy a new popular product and release a clone, today the need for cloning products has disappeared. Today, startups and entire companies are being bought up for whatever money BlackRock and Vanguard provide to their wards.

In order not to compete with each other in the same market, each big5 CAD company chooses separate technological niches for itself and gradually buys up programs and any technologies in this direction.

For example, John Walker (the future CEO of Autodesk) offered Mike Riddle to buy Autocad in 1982 for only $ 15,000 (initially for $ 8,000), but Mike insisted on selling Autocad for $ 1 and 10% of the product sales. In 2020, Revit became Autodesk’s top-selling product, which it bought in 2002 for $ 133 million. And already in 2018, Autodesk paid almost a billion dollars ($ 875 million) for Plangrid (a startup application for a tablet), where Carol Ann Bartz, the former CEO of Autodesk, became one of the board members several years before the purchase.

Thus, at the moment, the whole world of design and, in general, all the technologies of the world are divided into those who belong to Blackrock and Vanguard, and those whom these funds through their CAD branches have not yet had time to buy. No organization with high monetary performance has the opportunity to avoid meeting such financial giants, no matter in which country it is located.

Today it is no longer possible to build a new Autodesk or Trimble in our world, where with the resources that investment funds have today, you can buy entire countries, not to mention talented development teams.

We have removed all competitors from the market, but why are we not moving forward?

! There is no way to demonize the structures that were built by BlackRock and Vanguard: any organization and most likely every person on earth, having such “free resources and access to the printing press”, would take advantage of this and do exactly the same on the Blackrock site buying everything in its path.

In contrast to monopolies, only the world of open source solutions could today compete with such oligopolistic conglomerates. Let’s look further at how large corporations are trying to control the open source movement.

Why do global CAD vendors need thousands of database specialists, open source solutions, as well as solutions developed by the main CAD vendors, let’s talk in the seventh part.

In order for the seventh part to understand a little better the new player in the CAD market — Oracle, databases and open source, as well as due to the similarity of the behavior of the two companies — compare the history of Oracle with the history of Autodesk and look at how these two corporations fought open source movement on its market.

Autodesk is following in Oracle’s footsteps

The history of Autodesk, one of the leaders in the CAD world, is beginning to resemble the story of such a leader of its time as Oracle. Just as Autodesk and Autocad were the world leader in 2D design for the last 30 years, Oracle, at the same time, was the world leader in databases — DBMS systems (database management system).

Oracle’s profit from a data storage business is about 10 times more than sales of the leaders in the CAD industry: Oracle’s annual turnover today is $ 20 mlrd., While Autodesk’s is only $ 1.7 mlrd. Like all technology companies in the world , the leading shareholders of Oracle (as well as Autodesk, Trimble, Apple, Microsoft and almost every company on earth) are the two largest investment companies in the world — Vanguard and BlackRock.

Many articles say that Oracle was founded in the “late 1970s” and that Oracle “sells a line of software products that help large and midsize companies manage their operations.” But the fact that Oracle has always been a significant player in the national security industry is somehow ignored everywhere. And that its founder would not have earned his billions if he had not helped create the tools of modern state and world surveillance.

Just as many major post-Cold War growth companies owe their development to federal and defense contracts, Oracle actually takes its name from the 1977 CIA project codename. And it was the CIA that was Oracle’s first customer.

In the mid-2000s, Oracle began to take an active interest in the construction industry. Notably, Oracle became a strategic partner of buildingSMART in 2019, one year before major CAD maker Autodesk joined buildingSMART in 2020. Oracle is well positioned to become a leader in BIM technology. We will talk more about this and why BIM is a database in the seventh part.

At some point, large technology companies grew into large structures, which, like all large and complex structures, once stopped actively developing new technologies.

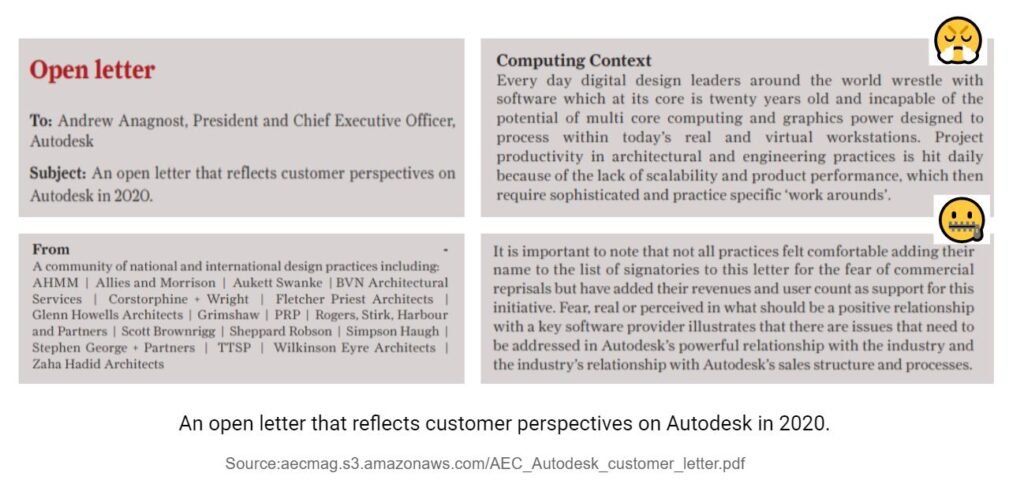

Both in the open letters of the world’s best architects addressed to Autodesk (more on this in Part 4: The Struggle between CAD and BIM. Monopolies and Lobbyists in the Construction Industry), and in the podcast with Elena Slepova — we all note that Autodesk hardly develops the main product Revit, but deals only with the design and decoration of the interface, along the way buying new startups (Navisworks, Assemble, Vault, Civil 3D) and technologies.

An open letter from the architectural bureaus of the Autodesk world that the Revit product is not developing.

The annoyance of designers with Autodesk products grows from version to version, but large corporations such as Autodesk, Nemetschek and other large start-up buyers cannot make significant changes to the code of the purchased programs.

Why programs don’t develop

Any large software product that has been in development for over five years is like a long spaghetti code. However, only a few top developers in the company know how (maximum) 70% of the code works in a program such as Oracle Database, Autocad, Revit, or Archicad. New tools from Autodesk, Nemetschek or Oracle today are just an attempt to hide accumulated problems from developers, because it has become impossible to cope with them.

The decline of active growth in technical terms begins with the departure of developers to higher positions or, more often, with the “Exit” of the main developers who take money (after the sale of the startup or the company’s IPO) and become venture capitalists themselves.

After the Exit of the main developers, a large number of crutches that make up these programs, in subsequent projects create hard-to-detect bugs that fill up all further product development. Such a product, or, more precisely, the code of which it is composed, is referred to as legacy code.

Legacy code (from Legacy (English) — inheritance) — a stable expression denoting an old code without any explanation; its main feature is the lack of the ability to understand it.

Legacy code is not a problem — if you don’t need to change it

Using Oracle as an example, you can imagine what is the complexity of Legacy code and why programs from the 90s have hardly evolved lately.

The Oracle Database codebase was 25 million C lines during development of version 12.2 in 2017 — and if you change just one of those lines, thousands of previously written tests break. Over the years, several generations of programmers have worked hard on the Oracle Database code, regularly chasing hard deadlines, making the code a nightmare.

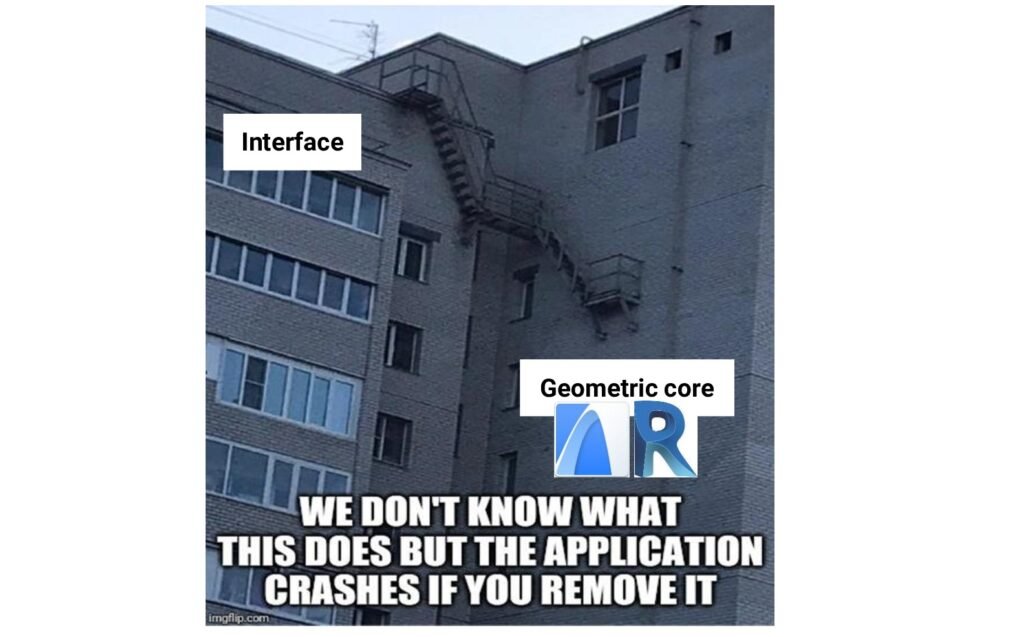

Interface — Geometric core. We do not know how it works, but if you uninstall this application it will crash

Today, the code of any program from the 90s consists of complex “chunks” of code responsible for logic, memory management, context switching, and much more; they are connected to each other with thousands of different crutches. As a result, it may take a developer a day or two just to figure out what a particular line of code actually does.

The question arises: how, with all this, Oracle Database (or Revit, Archicad) still manages to stay on its feet? The secret is in the millions of tests. Their full execution can take from 20 to 30 hours (while they are performed distributed on a test cluster of 100–200 servers), so today the process of fixing a single bug in Oracle Database takes from several weeks to several months.

Likewise, any closed product that has been in development for more than 5 years automatically becomes a “spaghetti code”, which can only move on crutches to its next version.

Autodesk develops Revit easier: developers simply do not deal with the topic of performance, and from version to version they create only those tools that work on top of the main functionality.

Since the main code was written in the late 90s, Revit uses only one processor core (excluding rendering), which hinders design performance. For example, Revit no longer has the ability to multithread using all the cores in the hardware. And even if in 10 years you will have a thousand cores in the processor, you will not get a performance gain in Revit.

Thanks to the constant turnover in addition to the problem of closed code development, we are full of old Legacy products that are terribly poorly written but are incredibly difficult and expensive to keep afloat today. Moreover, it will never be possible to rewrite them, because they interact with the same terrible code from product users, and therefore it is necessary to maintain compatibility with bugs and undocumented features. For this reason, many products have become hostages of backward compatibility. Including Windows, Microsoft Office and the main programs in the CAD market.

Programs such as Revit, ArchiCAD, Microstation no longer have a future, and perhaps the vendors themselves understand this.Therefore, all the forces of corporations today are spent not on increasing the productivity of the geometric kernel, but on finding a new successful product or new unique developers, like Leonid Raiz (Revit), Mike Riddle (AutoCAD) or Gabor Bojar (ArchiCAD).

Due to the lack of new successful products, the main efforts of such large corporations are beginning to focus on imposing their products, aggressive marketing and maintaining the current resource-intensive life support of a complex and bureaucratic structure.

The Campaign for Clear Licensing study found that audits by software vendors such as Oracle and Autodesk (Microsoft, SAP, IBM) block competition and discourage innovation in the IT departments of the companies where the audits were conducted.

Who is the least useful vendor in terms of auditing? Oracle was ranked as the worst vendor in the audit process, followed by IBM and Autodesk.

By the early 2000s, major corporations had carved out their niches in the industry and were quietly distributing profits to shareholders every year. But with the beginning of the open source era, a new competitor appears on the horizon — developers of open and transparent products, not at all like contract specialists who have moved to California or Boston from Asia or Europe.

By the mid-2000s, the main headache for the heads of large corporations Oracle, Microsoft, SAP, Autodesk, IBM is not a million lines of “spaghetti code”, but new open source products that are rapidly gaining popularity: Linux, GitHub, Spark, Mozilla, Gimp, PHP , WordPress, Android, Blender and thousands more.

In the case of Oracle, such a competitor was a young open source startup from Sweden — MySQL.

The corporation’s fight against open source

Usually any startups standing in the way of corporations could already be bought with the support of BlackRock by the beginning of the 2000s, but how to buy an Open source idea, behind which hundreds of developers from all over the world stand?

MySQL is an open source project that was simultaneously developed by hundreds of specialists from all over the world. At the same time, the code is completely free and transparent for further development (or writing tools for it), thanks to which MySQL quickly gained popularity in the database market.

In the struggle for the market, Oracle began to cut prices and provide large discounts to those companies that already used or were just about to use MySQL. At the same time, Oracle, realizing the threat to its business, tried in every way to buy this fast, free and transparent DBMS solution.

Throughout 2006, Larry Ellison (the head of Oracle with Odessa roots) repeatedly offered to buy MySQL, but three Swedish friends, the founders of MySQL, constantly rejected the offer from the “evil empire” Oracle, which took off thanks to cooperation with the CIA.

As a result, the shareholders of MySQL sold their product to Sun (the founding fathers of MySQL received $ 10 mln from the deal) and in 2009 Oracle managed to outstrip IBM and signed an agreement to buy Sun (along with the MySQL product) for $ 7.4 billion.

In 2009, MySQL had a big update: MySQL 5.4 added support for 16-processor x86 servers, and, according to some tests, MySQL performance should have increased tenfold. MySQL 5.4 was slated to ship on April 21st, but by coincidence there was a deal with Oracle the day before.

After the purchase, in order not to give development to its rebellious open source foster son, since 2009, Oracle (which now owned the rights to MySQL) tried to shake and slow down the open development model of the famous DBMS from the inside.

Thus, Oracle, with the help of BlackRock, cleared the market for its main proprietary “spaghetti product” Oracle Database for the next 10 years, and the shareholders of investment funds could now expect to pay dividends at the expected level in the coming years.

But the open source MySQL idea can no longer be killed, and developers from the MySQL community began to flow into other open source projects. As a result, all the main MySQL developers gave up on Oracle and switched to faster and more modern open source databases — MariaDB (a fork copy of MySQL), PostgreSQL and SQL-lite.

Similar purchases are constantly taking place in the CAD market. All the same trends await any CAD and BIM solution developer, and the story with MySQL itself is similar to the story with IFC, which was originally an open format.

Oracle has essentially done with MySQL what Autodesk did with IFC in the mid-90s, but much faster and easier.

Autodesk and IFC data format

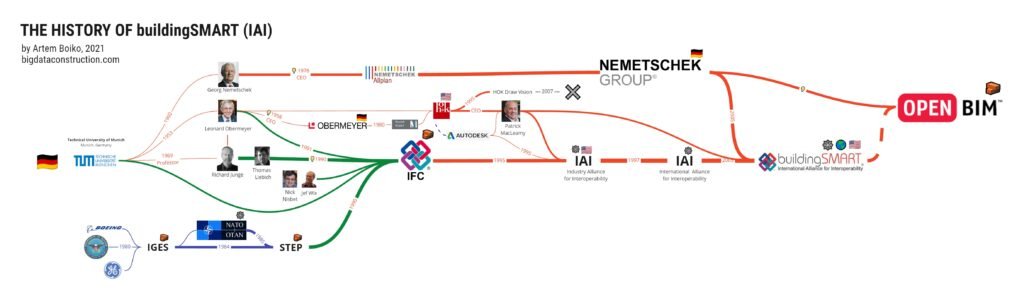

The idea of an open format for IFC was born from the visionary of construction technologies Leonard Obermeyer, who, prior to the Olympics in Munich, during the construction of Munich Airport, interacted with suppliers and companies from all over the world. During the design of the Olympic projects, Leonard Obermeyer realized that there was a need for one common language in which builders and manufacturers of building elements from all over the world would communicate.

Since Leonard Obermeyer himself was not a programmer, he passed this idea on to his home faculty at the University of Munich, where Richard Junge and Thomas Liebich with a team of students were further developing the new open format.

The idea of the creators of the IFC format was to create a worldwide and free language for data exchange in construction (despite the military roots of the IFC-STEP format, Application Protocol 225), but in the early 90s, little was known about open source.

Thanks to Leonard Obermeyer’s friend Patrick MacLeamy (CEO of HOK), Autodesk is actively involved in the “development” of the global IFC idea. Only a few years pass, and Autodesk takes full control of IFC registration and development.

More on this in Part 3: The Fathers of BIM Technologies. Who is behind the success of Autodesk and openBIM?Lobbyistenkriege und die Entwicklung von BIM.

In diesem Artikel werden wir die Arbeit aller “großen Väter” der BIM-Technologie hervorheben, die in den 80er und 90er…boikoartem.medium.com

But by the end of the 90s, not having normal 3D products, Autodesk itself could not use this product normally in its programs — and the idea of a “world 3D format” was being taken over by the IAI cartel organization (which was later renamed buildingSMART).

Patrick MacLeamy, Autodesk’s joint project partner with HOK (where McLeamy was CEO), remains at the helm of buildingSMART to oversee the development of IFC. By the way, in some countries even today representatives of Autodesk and representatives of buildingSMART are often the same specialists.

Based on these facts, it can be assumed that the American organization buildingSMART keeps Autodesk aware of possible “development options” so that Autodesk can seize the initiative in the world of data exchange formats in time and engage in new technologies without looking at competitors.

Similarly, Autodesk released Dynamo, an open source solution that Revit and Civil 3D use to extend functionality. Dynamo was originally introduced as an open source product that suddenly appeared in 2011 in the bowels of Autodesk (or rather was developed by Luke Church for Autodesk). Just like buildingSMART, which Autodesk had a hand in its birth, Dynamo code is also not very transparent. Many developers point out that packages wrapped in DLLs often deny access to the code, which prevents users from examining the code or how individual pieces of code are processed or analyzed in Dynamo. This also prevents Dynamo from being used in truly open source products such as BlenderBIM (Sverchok is used for visual programming in Blender today).

Thus, Autodesk, in control of open IFC and Dynamo projects, created a construct similar to the one that Oracle created with MySql. Only in the world of databases — Oracle “openly”, through Sun, bought open source — MySql, and Autodesk remotely controls the movement of Dynamo and buildingSMART projects (which, in turn, tries to communicate remotely with European vendors of the openBIM movement — Nemetschek).

And if today a truly new open source format is formed or Revit has a worthy open source competitor, then Autodesk will follow the proven path of Oracle and, possibly, try to buy out the rights to any product at the earliest stages, which, most likely, will again prolong life Autodesk products for another decade.

Today buildingSMART is slowly trying to set the rules in the CAD market, while buildingSMART’s interests are mainly dictated by the needs of the main players in this niche — Autodesk, Bentley Systems (since 2019 Oracle).

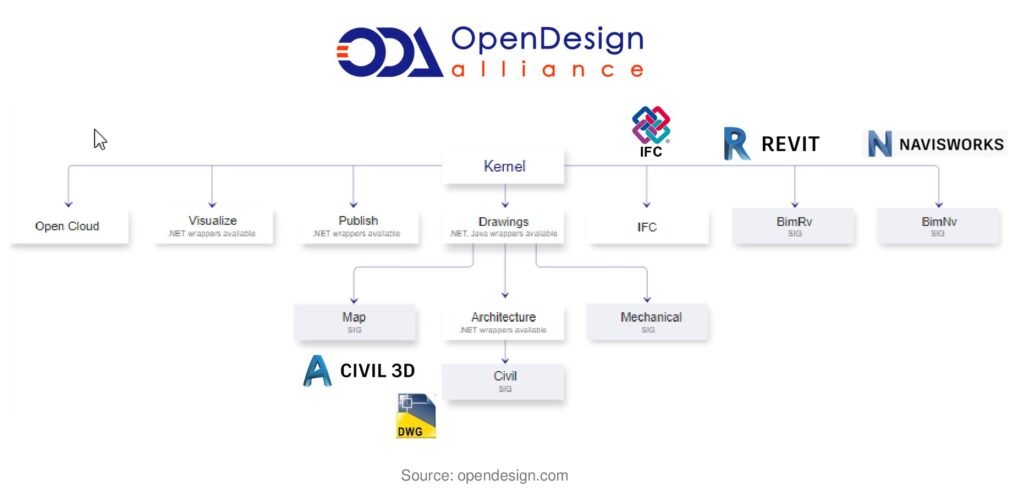

The only organization more or less free from lobbying is the ODA (Open Design Alliance).

Autodesk Challenge — Open Standards Organization — ODA

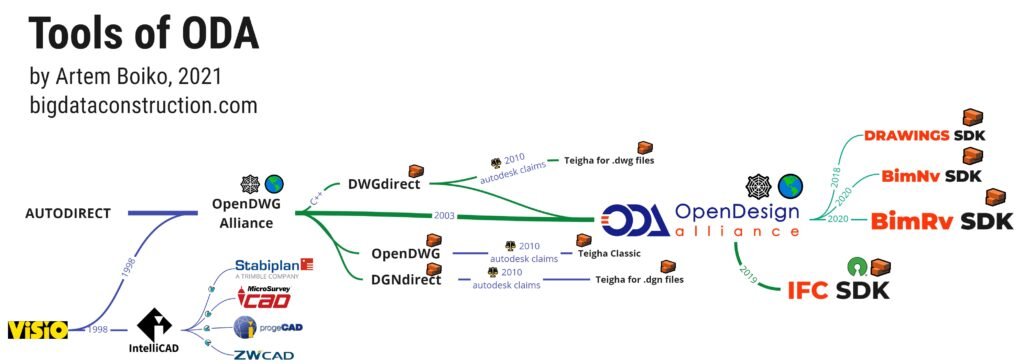

ODA made a big difference for CAD users around the world when it allowed CAD developers to dramatically reduce the cost of supporting the DWG format, which has become the de facto industry standard for CAD data exchange.

ODA has created products (of which Teigha is the main one) with the ability for more than 2,000 member organizations to operate without regard to Autodesk, effectively removing the artificial barriers that have held back the entire CAD industry.

The Open Design Alliance is a non-profit consortium dedicated to the dissemination of open formats for the exchange of CAD data.The ODA technology platform provides users with the means to create a wide range of applications, including visualization tools and even full-scale CAD systems. The platform supports DWG, DGN, NWD, NWF, NWC, RFA, IFC, RVT files with editing, import and export capabilities in other file formats.

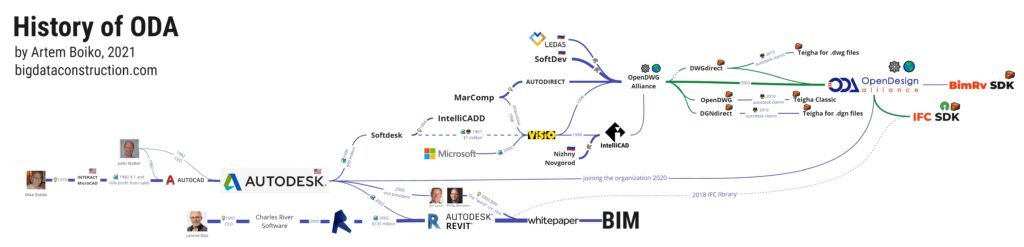

The history of ODA began with an attempt by Autodesk to buy SoftDesk, which in the mid-90s developed its CAD platform with the goal of completely replacing AutoCAD. After an antitrust investigation, the court banned Autodesk from buying SoftDesk, which later (after the transfer of rights to VISIO) was bought by Microsoft.

In 1998, a new alliance, OpenDWG, was formed on the basis of technologies from Softdesk and InteliCADD (later InteliCAD). The OpenDWG Alliance (ODA) is committed to leveling the playing field for all CAD vendors, regardless of their relationship with Autodesk.

The first conflict between ODA and Autodesk arose in the early 2000s over the DWG format.

In 1998, ODA provided new tools to millions of software users with the ability to continue to use the DWG file format without being tied to a single vendor, Autodesk.

It is noteworthy that the DWG file format itself and the Autocad program were developed by Mike Riddle and that DWG was used in the late 1970s in his InteractCAD, and only in 1982 John Walker bought out the entire Autocad product along with the DWG format, thus founding Autodesk for mass production of DWG product sales.

Autodesk itself, after purchasing the Autocad program (20 years), did not provide an API for accessing DWG files, therefore, the answer to such closeness was the appearance on the CAD market of the first open initiative: GNU LibreDWG, which could read the DWG format. Unfortunately, LibreDWG could not edit the information in the DWG file.

This barrier to modify the DWG file was overcome by ODA’s alliance with Teigha, which allowed DWG to work in any CAD program. This product has leveled the chances of all CAD developers, and such well-known companies as the Belgian Bricsys, the German Graebert, the French DraftSight, the Chinese ZWSoft, the Russian NanoSoft and a number of others owe their success to him.

In response to open source development, Autodesk created a tool for third-party CAD developers — RealDWG (true true DWG) in the form of export and import modules, which allowed third-party CAD developers to finally embed export and import of drawings in DWG format into their functionality.

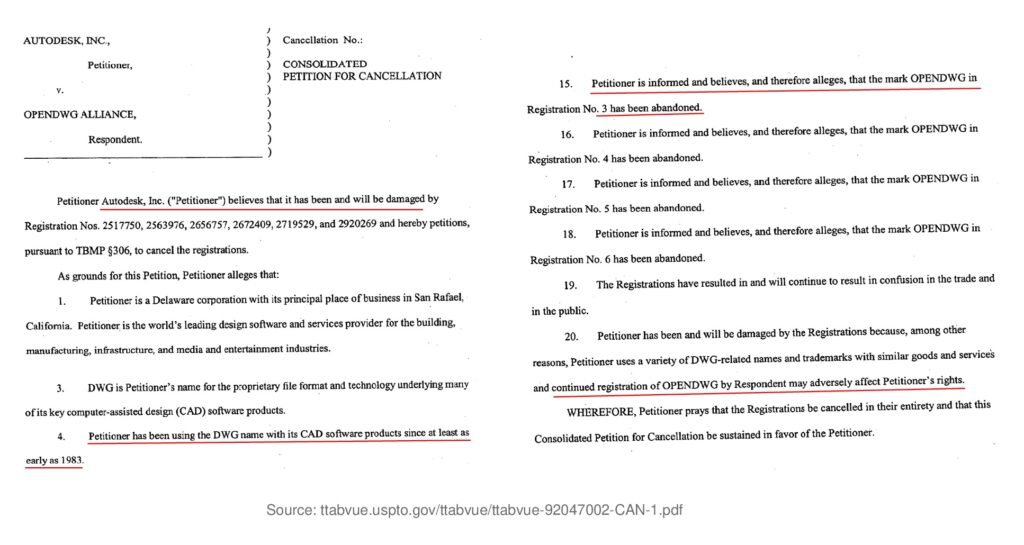

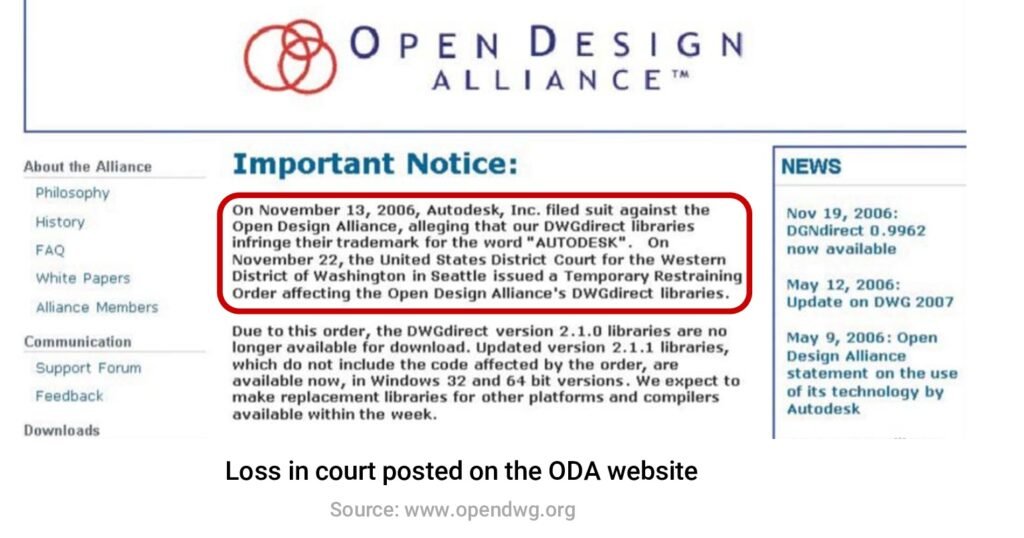

Since 2006, lawsuits have rained down on ODA from Autodesk, which was trying to protect the DWG product they bought in 1982. And since confronting the ODA, in order to complicate the life of competitors and artificially limit competition, Autodesk has created a new version of the “most correct” DWG format every few years (while inserting Autodesk’s “watermarks” into the format).

In 2006, Autodesk introduced TrustedDWG technology into the updated DWG 2007 format, which determined whether a DWG file was created in one of Autodesk’s products or in a program using RealDWG. In case the DWG 2007 file was created in an unlicensed program, AutoCAD would display a message warning the user of possible compatibility issues. The company motivated its decision by taking care of users.

Due to the keen interest of competitors in ODA tools, 25 years after the creation of DWG, Autodesk decided in 2006 to register DWG as its trademark. Having taken over the CAD market, Autodesk argued that only Autodesk products could make the “most accurate DWG” file.

Autodesk won the courts, and at first glance, it seemed that Autodesk defended its rights to the DWG format, but injunctions were not the end of the world for the ODA alliance.

In 2007, the lawsuit was finally withdrawn. The parties entered into an amicable agreement. ODA removed the TrustedDWG code from DirectDWG libraries, and Autodesk changed the warning messages in AutoCAD 2008. As a result, the court decisions only referred to the “DWG” trademark, while the DWG file format remained publicly available.

Perhaps today a similar struggle is unfolding for the RVT and RFA formats. The possibilities for creation in BimRv are still limited, but 100% of the data from the file is available for reading.

Revit (and a similar fork of PTC — Solidworkds) and the RFA and RVT formats were developed by Leonid Raitz (and his PTC teacher, Samuel Gaisberg) in the 90s. After purchasing through patents and registering trademark rights, Autodesk tried to secure its rights over the 3D CAD software Revit and its format.

In May 2020, at the peak of interest in the Revit product and its BIM solutions (and not at the decline of popularity, as was the case with Autocad), ODA officially goes to market with its BimRv SDK product. ODA’s BimRv SDK offers Revit data independent of the Revit application. The tool allows, for example, to create families (type geometry) without using Revit.

A few years before the publication of the BimRv release, ODA becomes the first vendor that not only allows you to read information from IFC, but makes it possible to create IFC geometry, which no CAD company has been able to do yet. ODA’s complete open source IFC toolkit will provide data access and object creation, integrated with high-speed rendering and the ability to convert IFC data to other formats such as .dwg.

It is logical that if a tool that edits Revit or IFC files from ODA gets real distribution, then the profits that Autodesk makes on its products today could plummet..

Based on the experience of fighting Softdesk and after litigation with ODA over the Teigha-DWG product, Autodesk understands that ODA with BimRv SDK has already advanced an order of magnitude further in its capabilities, and now ODA will no longer make mistakes that were made in the struggle for the openness of the DWG format …

Therefore, today Autodesk is left to massively buy new technologies in the start-up market or try to “complicate” the work of the ODA alliance, which is trying to “illegally” (according to Autodesk) distribute RVT and DWG formats and, along the way, become the revived SoftDesk, which Autodesk did not succeed kill to the end at the very beginning of development.

“The easiest and surest way to deceive a person is to pretend to be a friend.”

Publius Ovid Nazon

Watching ODA’s success from the outside, Autodesk made a strong decision to join the ODA alliance in order to get the best possible understanding of all the possibilities of an alliance that has not yet been purchased. Autodesk indicated the reason for joining ODA: interest in ODA’s IFC toolkit (which provides full and flexible IFC compatibility for any desktop or web application). At the same time, Autodesk joined the buildingSMART organization itself, which deals not only with IFC tools, but also the development of the IFC format itself one month later, in October 2020.

Due to the activity of the ODA alliance on the disclosure of RVT formats, RFA, starting in 2020, Autodesk began to actively return to managing its abandoned adopted son — the IFC format, embedding from the Revit-2020 version all those export capabilities to the IFC format that were previously (apparently , artificially) were inhibited or simply did not develop.

Perhaps Autodesk realizes that proprietary formats today will no longer be able to drive the business model that was successful in the 90s, and therefore today Autodesk aims to abandon formats and sell mainly cloud solutions. At the same time, Autodesk is in a hurry to lead the development of open technologies in the CAD world, following its friends: IBM, Microsoft, Oracle, SAP, who have also declared their rights to leadership in open source development (more on this in the next part).

But open source does not fit well with the policies that Silicon Valley firms have pursued over the past 30 years.

In conclusion

The times of real competition “thanks to” financial funds are going down in history. The lack of competition affects the development of technology in our already backward construction industry.

Old corporations such as Autodesk, Hexagon, Nemetschek Group, Trimble, which built excellent infrastructure in the 90s, are trying to adapt to the rapid changes in the market. Development of Legacy software such as Revit and Archicad is slowing down. Small CAD and BIM startups are either destroyed, or bought for a couple of million (or like Plаngrid, Aconex already billions) dollars — and go into the bureaucratic system of deadlines and crutches; and corporations seem to have neither the interest nor the creativity to develop new ideas and tools on their own.

The software crisis in CAD and other technologies is also systemic and generational in nature. The problem is that now at the helm of BlackRock, Vanguard, Oracle, Autodesk and other companies are Generation X or Baby-Boomers who still remember the decolonization of the dominions and the Caribbean crisis in the 60s.

And, of course, we cannot help but have respect for this generation (our parents), but it is obvious that technology is developing too quickly to give control of new technology to people from BlackRock or Autodesk who were born at a time when a person had not yet invented the remote control. from the TV, and the computers were about the size of a house.

In general, the consolidation of capital and the monopolization of the market with further construction of oligopolies or direct monopolists is a natural course of capitalism. Thus, capitalism on steroids has created a management bureaucracy or, in other words, a planned economy at the global level.

Only if in the Soviet Union, under a planned economy, the profit received belonged to all members of society, then in the world planned economy, only shareholders of basic investment funds receive profit.

Under no circumstances should the structures built by BlackRock and Vanguard be blamed for greed: in their place, any organization and possibly anyone would have done the same. We can be grateful to them for the fact that it was they who chose this dead-end path.

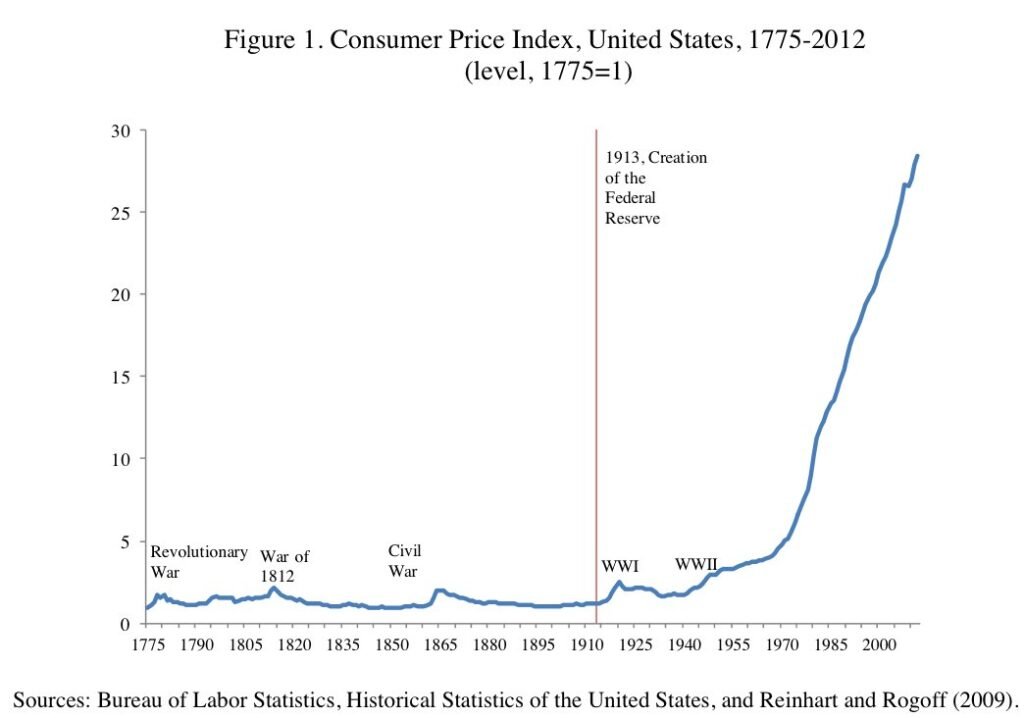

The constant increase in the prices of startups and such an amount of free money in investment funds in the world is associated with lower interest rates around the world since 1980. The following graph shows the median interest rates in the world over the past 200 years, which until 1980 were around the world at a balanced and reasonable level: about 4–6%.

The lowering of interest rates and the decoupling of the dollar from the gold standard in 1971 led the world to inflation, which became a phenomenon of the 21st century.

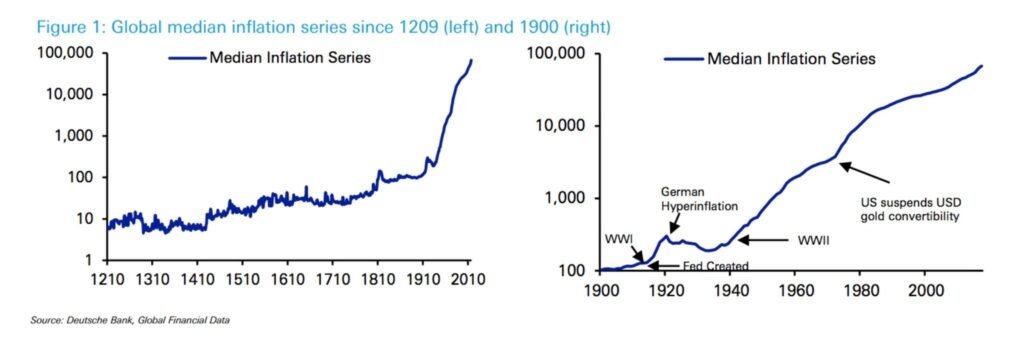

The same phenomenon from German analysts at Deutsche Bank.

Therefore, the amount of available funds for the purchase of companies, entire corporations and technologies in the accounts of investment funds today will increase quarterly in parabolic growth.

Problems and crises help us. Large corporations, thanks to the continued support of Mom BlackRock and Dad Vanguard, are not able to create difficult times for themselves that could help companies and technologies move to the next level of development.

“ The one is no longer cunning, about whom everyone says that he is cunning.“

Alexander Suvorov

It is logical that BlackRock and Vanguard will go down in history with their bureaucracy and complex closed structures, just as this bureaucracy and vertical communication system disappeared from the planned economy of the Soviet Union. All that is lacking to defeat BlackRock and Vanguard is the strong rival that a decentralized economy could become today.

Perhaps because of such funds of the conquistadors, who sail across continents on the Vanguard ship today (as it was already in the 13–18 century) and buy up the most interesting and important sources of knowledge, local developers (for example, from Asia) will be able to rally for independence from this big money protectorate. Therefore, the stronger the pressure of funds becomes, the more powerful the symmetrical response of the decentralized world will probably become.

Thanks to the transparency of information: to journalists, the advent of cameras and cameras — at the end of the 20th century, people stopped killing other people en masse. And in the 21st century, thanks to the Internet and decentralized applications, a new decentralized economy is being created before our eyes with the help of open source code, which old corporations and their friend BlackRock are trying to keep up with.

These many Western companies and structures still have their own restructuring and publicity in the future.

“ The real indicator of your wealth is what you will be worth if you lose all your money..“

Unknown author

We can only hope for crises and black swans like COVID-19, thanks to which specialists from all over the world after 2021 may stop rushing to move to other countries and look for their place in this, albeit monetary, but very bureaucratic and outdated structure. Such new and unique specialists, such as Gabor Bojar, Mike Riddle, Samuel Geisberg, can already today develop new CAD-BIM technologies from anywhere available.

The new world of software and technology will be much more transparent, thereby contributing to an increase in the number of developers, the creation of new remote jobs and the opening of new opportunities for monetization.

We will talk about open source solutions, monetization, and why IFC is not open source in the next part.

I would be grateful for the repost on social networks and would be glad to receive your comments, clarifications and criticism.

The link diagram of the BIM programs indicated in the article in good quality is available at the link (shareholding schemes are located on the page in Miro)

History of BIM:

📰 Previous related articles:

⚈ Lobbyist Wars and BIM Development. Part 4: The fight between CAD and BIM. Monopolies and lobbyists in the construction industry.

⚈ Lobbyistenkriege und die Entwicklung von BIM. Teil 3: Väter von BIM Technologies. Wer steht hinter dem Erfolg von Autodesk und openBIM?

⚈ Expat Network. Comparison of construction, BIM and 5D Design in Asia and Europe : KAZAKHSTAN, UKRAINE, AUSTRIA, CHINA, GERMANY

⚈ Inflation and profitability in the construction industry. Rising costs of work in San Francisco.

⚈ Trends and History of the Construction. The Ups and Downs of the San Francisco Construction Industry.

⚈ The Construction Industry is dying out. Covid-19 crisis growing Сhallenges and Opportunities.

⚈ Can you earn more in another country? Engineering Salaries Worldwide.

🚀 Level Up for BIM-Engineers of any level

📈 If You work in Construction with BIM und you need to understand Big Data, Machine Learning, 4D and 5D in Construction . Then these courses are for you:

Machine Learning in Construction. Price and Time Prediction

We will examine in detail the basic types, terms and algorithms of machine learning. We go through the basic concepts of machine learning that beginners need. We will consider in more detail such algorithms as K-means supervised Machine Learning, Linear Regression and other algorithms for Machine Learning.

✔️ In practical lessons we will predict the time and cost of construction for the new project X, based on the data that we collected on previous projects. And in another lesson we will predict the cost of building project X and construction time by the parameters that we will set for the new project x

✔️ Then we take open source data for the San Francisco city. We will clear this raw data and display the data in the form of a charts and maps. We will collect various interesting insights from this public information. Then we will prepare the data to create a machine learning model and try to #predict some parameters from this data.